Before you sign a commercial lease, you sign something shorter and far more important than most tenants realize. A letter of intent for a commercial lease is the two- or three-page document that sets out the deal before the lawyers turn it into forty pages of contract. Get it right and the lease that follows is on the path to being a formality. Get it wrong and you could spend the next month or so trying to claw back ground you gave away in the first draft.

This guide is written for tenants: what the letter of intent does, what belongs in it, and the one trap that catches people who treat it as a casual first step. Where it helps, there are notes on what the landlord is looking for, because knowing the other side’s read is half of negotiating well.

Key Takeaways

- A letter of intent (LOI) sets out the business terms of a lease before the formal contract is drafted.

- It’s non-binding overall, but the terms inside it set your economic ceiling. Reopening one later is expensive in goodwill and leverage.

- Lock the economics in the LOI: rent, term, lease type, TI allowance, free rent, and your options. Leave the legal machinery for the lease.

- Spell out which clauses are binding (confidentiality, exclusivity) and which aren’t, so there’s no argument later.

- Give the LOI the same attention you’d give the lease. Most of the deal is decided here.

What a letter of intent actually is

A letter of intent, usually shortened to LOI, is a short document that lays out the main terms a tenant and landlord have tentatively agreed on before anyone drafts a lease. Think of it as the deal in outline: the rent, the term, the space, the build-out money, the options. It’s the handshake written down.

It does a few things at once. It forces both sides to put real numbers on the table instead of talking in generalities. It gives the landlord’s attorney a framework to draft from, which speeds everything up. And it lets you settle the expensive questions before you start paying a lawyer to read a long lease line by line. That last point matters more than it sounds: negotiating the big terms in a three-page LOI is far cheaper than negotiating them inside a sixty-page contract.

What the landlord is looking for here: a serious tenant. A signed LOI tells the owner you’re committed enough to move forward, which is why they’ll often take the space off the market, or at least stop actively showing it, once one is in hand. That commitment cuts both ways, and it’s worth knowing you’re giving them something real by signing.

The binding-versus-non-binding trap

Here’s the part that catches people. An LOI is described as non-binding, and in the strict legal sense that’s true: signing it doesn’t obligate either side to complete the lease. So tenants relax, treat it as a rough draft, and figure they’ll fight the real battle when the lease shows up.

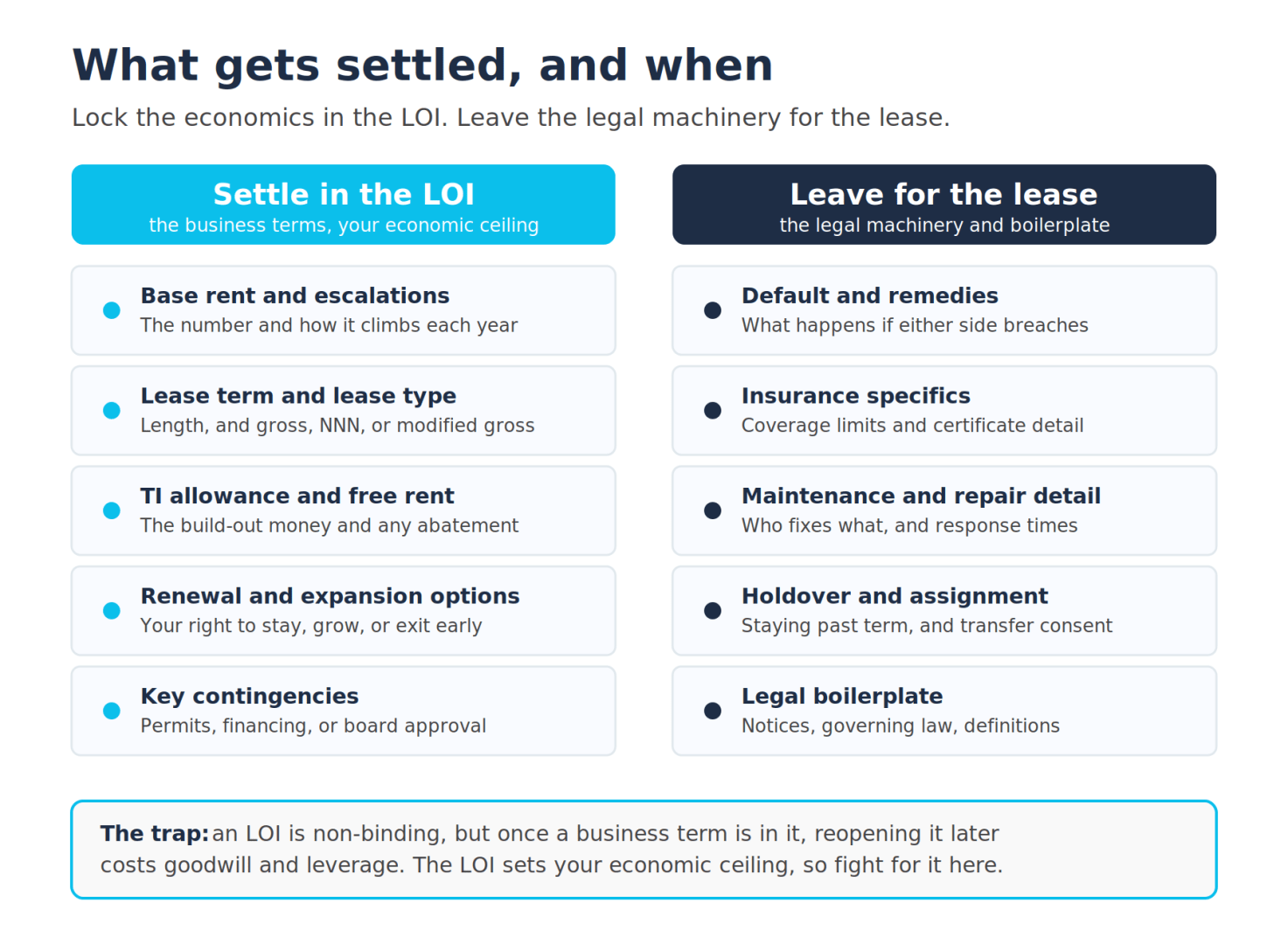

That’s the mistake. The LOI is non-binding as a contract, but the numbers in it become the starting point for everything that follows, and in practice they set your ceiling. Once you’ve agreed to $32 per square foot in the LOI, the landlord’s attorney drafts the lease at $32, and the landlord will resist reopening it. From their side it’s reasonable: the business people already agreed, so why are we relitigating it? Reopening a settled term doesn’t just cost you time. It costs goodwill, and it spends leverage you’d rather save for something else.

So the rule is simple. Treat every business term in the LOI as though it’s close to final, because functionally it is. The time to push on rent, on the TI allowance, on your renewal option, is now, in the LOI, not later when the lease arrives and everyone believes the hard parts are behind them.

What to settle in the LOI versus the lease

Not everything belongs in the LOI. The skill is knowing which terms to nail down now and which to leave for the lawyers to handle during lease drafting. As a rule, the LOI is for economics and structure; the lease is for the legal machinery.

Lock these in the LOI, because they’re the terms that decide what the deal actually costs you:

- Base rent and escalations. The headline number and how much it climbs each year. A one-percent difference in the annual bump adds up over a ten-year term.

- Lease term and lease type. How long, and whether it’s gross, modified gross, or triple net. The type of lease determines which costs you carry on top of rent, so it can’t be an afterthought.

- Tenant improvement allowance and free rent. The build-out money and any abatement. A larger TI allowance is often worth more than a month of free rent, so put a real number on it here.

- Options. Renewal, expansion, and early termination rights. These are far easier to win in the LOI than to add at renewal, when your leverage is gone.

- Key contingencies. Anything the deal depends on, such as permits, financing, or board approval. If it could sink the deal, it belongs in the LOI.

Leave these for the lease, where they’re properly handled in detail by your attorney:

- Default and remedies. What happens if either side breaches, and the cure periods involved.

- Insurance specifics. The LOI can note who carries what, but coverage limits and certificate detail are lease-drafting work. (The structure does follow lease type, so it’s worth understanding how that interacts before you sign.)

- Maintenance and repair detail. Who fixes what, and within what timeframe.

- Holdover and assignment language. The exact terms for staying past the lease end or transferring the lease.

- Legal boilerplate. Notices, governing law, definitions, and the rest of the contractual scaffolding.

The sections a commercial lease LOI usually includes

LOIs vary by deal and by sector, but most cover the same ground. If you’re reviewing one, or writing one, expect to see:

- The parties. The tenant (and any guarantor) and the landlord, named clearly.

- The premises. The building, the suite, and the square footage, with a note on whether that figure is rentable or usable, since the gap between the two affects what you actually pay.

- Lease term and commencement. The length, the start date, and any conditions attached to commencement.

- Base rent and escalations. The rate, the payment schedule, and the annual increases.

- Lease type and operating expenses. Gross, modified gross, or triple net, and how taxes, insurance, and CAM are handled.

- Tenant improvements. The allowance, who manages the build-out, and the delivery condition of the space.

- Concessions. Free rent, moving allowances, or other incentives.

- Options. Renewal, expansion, termination, and rights of first offer or refusal.

- Security deposit. The amount, and any burn-down provision that reduces it over time.

- Contingencies. Permits, financing, approvals, or anything else the deal hinges on.

- Binding provisions. Which parts of the LOI do bind, typically confidentiality and exclusivity, and an expiration date for the offer.

That last item is worth dwelling on. Even a non-binding LOI often contains a few binding clauses, and you want them spelled out plainly. Confidentiality keeps your terms private. An exclusivity or no-shop clause stops the landlord from shopping your offer to other tenants while you negotiate, which is genuinely useful to a tenant and worth asking for. State clearly which provisions bind and which don’t, so nobody argues about it later.

How to use the LOI to your advantage

Because the LOI sets the economic ceiling, it’s where your preparation pays off. Walk in knowing the submarket: what comparable space is asking, what’s actually trading after concessions, and how much vacancy the landlord is sitting on. A landlord with empty floors and a quarter to close is in a very different position than one with a waiting list, and the LOI is where that difference turns into terms.

Put an expiration date on your own LOI when you’re the one extending it, usually a handful of business days. It keeps the deal moving and stops the landlord from using your offer as a stalking horse for a better one. And give the document the same care you’d give the lease itself, because most of the deal is decided right here. The lease mostly formalizes what the LOI already settled.

One last point: an LOI is not a substitute for legal review. It’s lighter than a lease, but the terms in it carry real weight, so having an attorney or an experienced tenant rep broker look at it before you sign is time well spent. This connects directly to the negotiation work that comes next, and our guide to negotiating an office lease covers how to push on each of these terms once you’re at the table.

Frequently Asked Questions (FAQ)

Is a letter of intent for a commercial lease legally binding? Generally no, not as a whole. Signing an LOI doesn’t obligate either party to complete the lease. But most LOIs contain a few clauses that do bind, usually confidentiality and exclusivity, and the business terms inside, while technically non-binding, set the starting point the lease is drafted from and are hard to reopen later.

Who writes the LOI, the tenant or the landlord? Either can. In practice, brokers draft most LOIs rather than attorneys. A tenant rep broker often prepares it on the tenant’s behalf, while on the landlord’s side the leasing agent or the owner’s broker may extend it. Whoever drafts it, both sides negotiate the terms before signing.

What should always be in a commercial lease LOI? At a minimum: the parties, the premises and square footage, the lease term, base rent and escalations, the lease type, the tenant improvement allowance, any options, and a statement of which provisions are binding. Anything the deal genuinely depends on, like a permit or financing, should be listed as a contingency.

How long should an LOI stay open? When you’re extending an LOI, a short expiration window, often a handful of business days, is standard. It keeps the deal moving and prevents the other side from using your offer to negotiate a better one elsewhere.

Do I need a lawyer for the LOI, or just the lease? The LOI is shorter and less formal than the lease, but its terms carry real weight, so legal review is worth it at this stage too. An attorney or experienced tenant rep broker can flag a term you’d regret before it becomes the foundation of the lease.

Matthew Preston

Content Writer, CRE News & Market Analysis

Matthew has covered commercial real estate for CommercialCafe since 2022. He focuses on the office and industrial sectors, reporting on leasing, development, and investment across national markets and individual submarkets. His work draws on data and original research. He also writes about demographic shifts and urban innovation in U.S. cities. The New York Times, The Real Deal, Bisnow, The Business Journals, and Yahoo Finance have cited his reporting.